After a car accident, especially when the other driver is at fault, you’ll likely have to deal with their insurance company. This can be intimidating—especially when you’re already stressed about damage to your vehicle, medical bills, or missed work. Knowing your rights and how to communicate effectively can protect you from lowball offers, delayed payments, or denied claims. In this guide, we’ll walk you through exactly what to expect and how to handle the process like a pro.

1. Know Your Rights Before You Speak

You are not legally required to speak with the other driver’s insurance company. However, if you choose to do so, keep in mind that their goal is to protect their bottom line, not yours. They may try to minimize their payout or pressure you into accepting a quick settlement.

Before speaking with them:

- Review your own insurance policy

- Understand your state’s laws on fault and liability

- Consider speaking with a legal professional, especially if you suffered injuries

2. Be Cautious with What You Say

If you decide to communicate with the other driver’s insurer, stick to the facts. Avoid emotional language, assumptions, or admitting fault. Common mistakes include saying things like “I’m sorry” or “I didn’t see them,” which can be misinterpreted as admitting liability.

Helpful tips:

- Only confirm basic facts: time, location, type of accident

- Avoid discussing injuries until you’ve seen a doctor

- Never give a recorded statement without understanding the consequences

3. Don’t Feel Pressured to Settle Quickly

Insurance companies often offer quick settlements to limit their liability. These initial offers are usually lower than what your claim is worth. If you accept too early, you may not receive compensation for long-term medical treatment, lost wages, or other hidden costs.

Take your time:

- Get a full damage estimate for your vehicle

- Have a doctor assess any injuries

- Understand the value of your claim before agreeing to anything

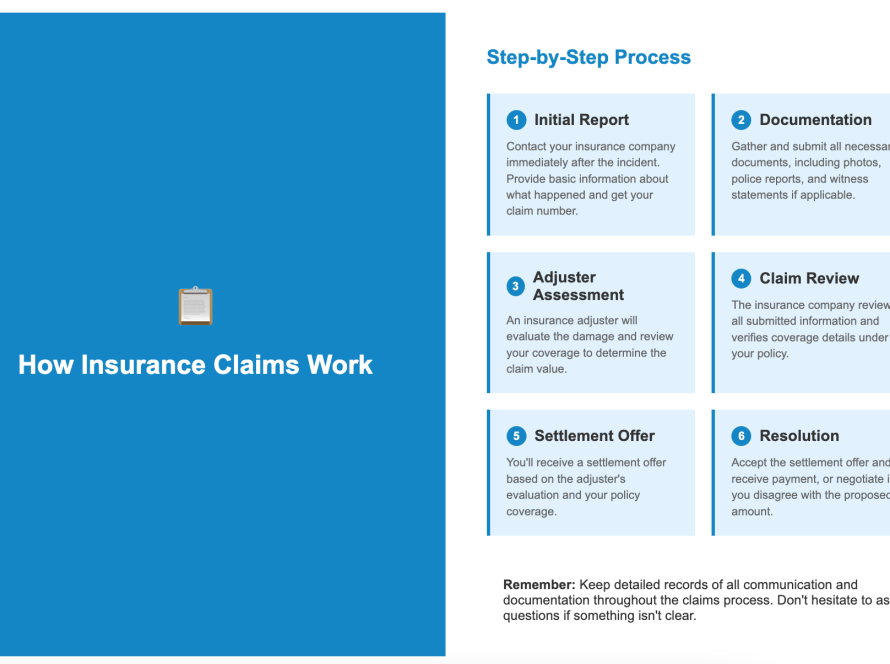

4. Document Everything

Keep detailed records of all communication with the other driver’s insurance company. Save emails, log phone calls, and write down names and titles of everyone you speak with. This can be crucial if your claim gets delayed, denied, or disputed.

Also document:

- Photos of vehicle damage and accident scene

- Medical reports and expenses

- Repair shop estimates and receipts

5. Let Your Own Insurance Company Know

Even if the other driver is at fault, it’s a good idea to inform your own insurance company. They can provide guidance, help you understand your rights, and even deal with the other party’s insurer on your behalf. If you have collision coverage, you might also choose to file the claim through your own provider for faster processing, then let them recover the costs later (a process called subrogation).

6. Watch Out for These Common Tactics

The other driver’s insurer may:

- Ask for a recorded statement to find inconsistencies

- Offer a low settlement before you understand the full extent of damage

- Claim your injuries aren’t serious or unrelated

- Delay the process hoping you’ll give up

Stay alert and don’t hesitate to seek help from a professional if anything feels off.

7. You Can Choose Your Own Repair Shop

You are not obligated to use the insurance company’s preferred auto body shop. You have the legal right to select a trusted, certified shop to perform your repairs. A good shop will help handle the insurance paperwork and ensure the job is done right—often with a warranty on their work.

8. Consider Legal Help If Needed

If the accident caused injuries, major vehicle damage, or if liability is disputed, you may want to consult an attorney. Many personal injury attorneys offer free consultations and only charge if you win the case. Having legal representation can level the playing field when negotiating with the insurance company.

Final Thoughts

Dealing with the other driver’s insurance company can be tricky, but staying calm, informed, and cautious will help you get the compensation you deserve. Don’t rush into agreements, avoid giving too much information, and remember—you have the right to protect yourself and your interests.